We’ve come a long way from barter methods and the early forms of currency our ancestors used to pay for goods and services. One of the earliest known uses of minted coins as a payment medium started around 600 B.C. in what is now western Turkey. China is credited with the invention of paper, and around 700 B.C. the Chinese started using paper money as an alternative to coins.

Europeans continued using coins until around the mid-1600s when banks started issuing paper “banknotes” that could be exchanged at the bank for their face value in silver or gold coins, or, used instead of coins to make purchases. In those days, banks and private institutions created and issued currency instead of governments, which are now responsible for issuing money in most countries. As trade increased among Europe, Asia, and the Americas, the use of paper currency flourished because it could be easily mass produced and was more convenient to transport.

Throughout the industrialized world, paper banknotes and coins minted from precious metals continued to be the preferred payment standard over the next 200 years. But merchants and others who exchanged money often found it inconvenient to withdraw and carry around large amounts of cash from their banks, giving rise to the use of paper checks as a replacement for cash. By the mid 1800s, the use of checks in the United States had grown rapidly and became the primary means of exchange for large transactions.

Fast-forward to 19th century America. The Western Union company introduced the first money transfer service through its telegraph network in 1871, and for the next several decades, “Western Union” was synonymous with state-of-the-art money transfer. By the 1980s, the company had expanded internationally and advertised itself as, “The fastest way to send money worldwide”—a claim they held onto until online banking technology became widespread.

While Western Union pioneered the first means of electronic money transfer, another payment “first” was about to change everything…

Cards And More Cards

“I want to say one word to you. Just one word.”

“Yes sir.”

“Are you listening?”

“Yes, I am.”

“Plastics.”

That exchange between Benjamin, the lead character in the 1967 film “The Graduate,” and a party guest, wasn’t about payment cards. But, given the proliferation of credit and debit cards in mid-century America, it may as well have been.

The first bank-issued charge card was created in 1946 by John Biggins, a Brooklyn, New York, banker. The Charg-It card quickly became a popular form of payment, but it could only be used at a small number of local New York businesses. Soon, other businesses like department stores and oil companies that owned gas stations began issuing their own company-specific “courtesy cards” throughout major metropolitan areas. Expanding on the buy now/pay later concept, in 1950 a financial executive named Frank X. McNamara founded Diners Club International and issued the membership-driven Diners Club card, a charge card that could be used at multiple restaurants. The Diners Club model caught on quickly, and in 1958 the Bank of America created what we now think of as the first modern credit card: BankAmericard, the first true all-purpose charge card that could be used at a variety of businesses.

By the late 1960s, banks and credit unions began issuing debit cards tied to customers’ checking or savings accounts. At first, customers could only use these cards to withdraw cash from automated teller machines (ATMs), so they were commonly known as “ATM cards.” As banking systems improved, debit card technology evolved into a system that was able to directly debit money from a customer’s bank account. Because using a debit card was more convenient than writing a check, more and more consumers started using debit cards, and in 1998, debit card transactions outnumbered the use of personal checks for the first time ever.

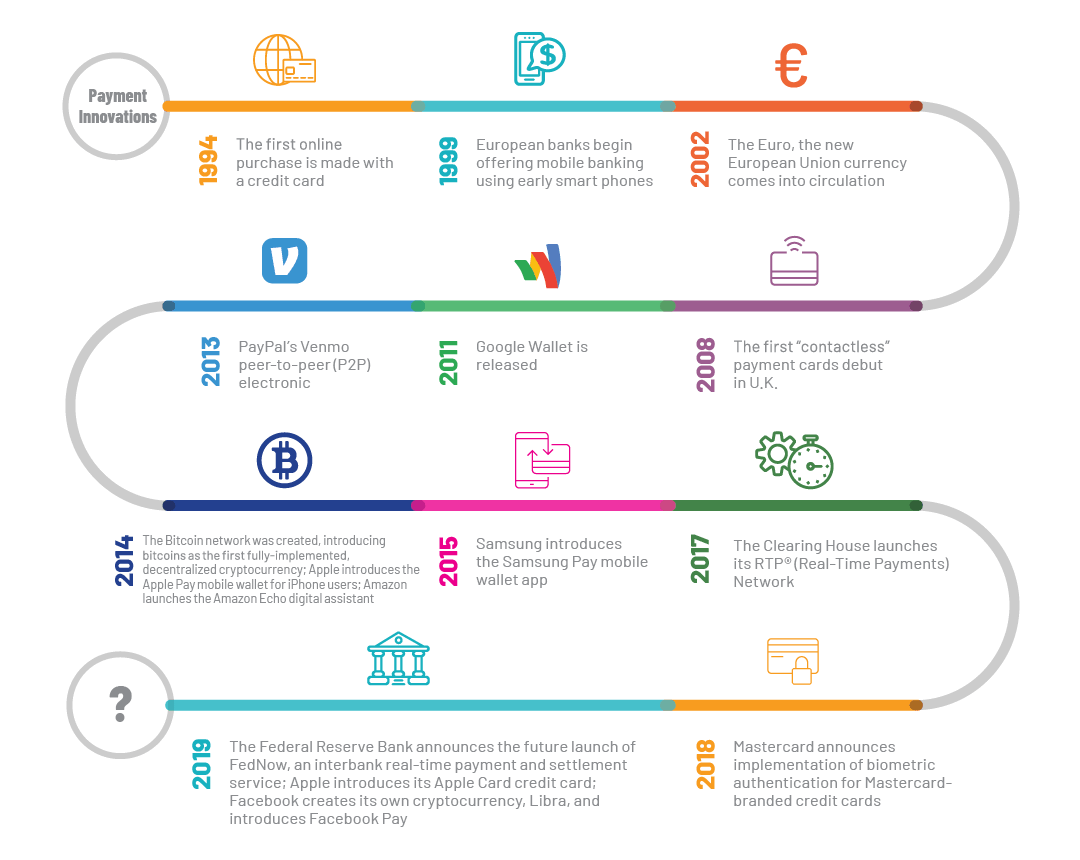

The first version of the EMV (Europay, Mastercard, and Visa) “chip” card was introduced in 1994. The chip card included advanced security features, but because the card technology required businesses to upgrade their POS systems to be able to process chip card transactions, it took several years for it to gain widespread use. Today, most major credit and debit cards are chip-enabled.

Cards Are Now the Payment Method of Choice

According to a Gallup study published in a 2018 article from The Ascent, a Motley Fool publication, 33% of Americans have one or two credit cards; 18% have three or four; and 7% have seven or more credit cards. Since debit cards are tied to checking or savings accounts, the average American consumer has at most one or two debit cards, but they have been a very popular payment vehicle, especially for small purchases. A 2016 consumer survey conducted by TSYS Merchant Solutions found that during 2015, debit cards accounted for $69.5 billion in payments, surpassing all other forms of non-cash payments including both checks and credit cards. The survey also showed that 46% of American consumers preferred to use debit cards at grocery stores and supermarkets instead of cash or credit cards; 39% at gas stations; 34% at discount stores; and 31% at department stores.

By the late 1990s, new forms of payment methods began to appear:

Business and Consumer Payment Methods

Merchants and consumers use many of the same payment methods for business or personal transactions, but some payment methods are primarily used by one group more than the other. For example, although cash is a common form of payment used by consumers, businesses typically use non-cash payment methods such as electronic money transfers when making business-to-business (B2B) payments to suppliers. Some businesses still pay their vendors and suppliers with checks, but check usage is declining.

For business-to-consumer (B2C) transactions, mobile and online card-not-present payments are becoming more and more popular. Consumers are writing fewer checks, partly because many retailers no longer accept them for payment (however, many small businesses continue to take checks because accepting credit cards is too expensive for them). Most businesses still take cash, and for many consumers, cash remains a preferred form of payment when making small purchases.

The following table lists common payment methods and indicates whether the method is primarily used for business or consumer transactions, or both. The table also highlights some of the advantages and disadvantages that come with each payment method.

Common B2B and B2C Payment Methods

From cash to credit cards to P2P money transfers, today’s shoppers can pick any number of ways to pay for their purchases. But with so many choices available, how does a buyer decide which one to use? Why would someone elect to use a debit card instead of cash to buy a latte? What makes a shopper decide to go to a retail outlet instead of making an online purchase? Does a sign at the cash register that says “No Personal Checks” cause a customer to pull a debit card out of their wallet, or just walk out the door? Knowing what influences a person’s decision to choose one payment method over another can help a business make it easy for customers to do business with them.

There is no “typical” American consumer. A person’s age, gender, occupation, geographical location, income, and education level, among other factors, all affect how purchasing and payment decisions are made. The products and services a person who lives in a large metropolitan area buys, for example, are most likely different from what someone who lives in a more rural setting typically buys.

The ongoing challenge for business owners is to understand who their customers really are so they can determine the best ways to attract new customers and keep their existing customers coming back. One way to do this is by analyzing statistical information that illustrates how different generations shop. The information on the following pages provides a snapshot of who today’s shoppers are, what they buy, and how they pay for purchases.

Seniors

This group is composed of people born between roughly 1925 to 1945. According to an article published by the National Aging In Place Council, by the year 2035 nearly one-third of all U.S. households will be headed by someone 65 or older, and 16 million households by someone 80 or older. These “active agers” are living longer and healthier lives than past generations, and they are retiring from work later in life. Older Americans today are a well educated, physically active, ethnically diverse group of consumers with money to spend.

While they do use a variety of payment methods, this age group pays for purchases using checks more than any other demographic. When it comes to plastic, 32% of seniors prefer debit cards, while 38% prefer using credit cards, with American Express being the most preferred credit card over any other. They’re also the least likely to embrace peer-to-peer (P2P) payments apps, online banking, or cryptocurrencies.

Key Takeaways:

Though seniors are definitely not a homogeneous population, they share some common attributes that merchants should keep in mind when marketing to this group:

- Retired seniors have more time to shop and they spend more time doing comparison shopping than other age groups.

- A lifetime of making purchases provides this generation with a high level of economic literacy (knowing the difference between the best price and the best value).

- Older consumers are less subject to peer influences than younger consumers and are less responsive to hyped-up marketing messages.

- Seniors are less likely to believe that there is as much difference between products that marketers like to claim.

- This demographic could account for more than half of all growth in urban areas in developed markets over the next 15 years.

Baby Boomers

The Baby Boom generation got its name because of the sharp rise in births following the end of World War II and is usually defined as those born between 1946 and 1964. Boomers represent the second largest generational group after Millennials, which makes them an important generation to watch—thanks to both their sheer size and the $2.6 trillion they collectively hold in buying power. Although a large number of Boomers are still working full time, in 2019 there were 73.4 million baby boomers in the U.S. who were either close to or already in retirement.

As Boomers age, they put more value on healthy food and active lifestyles. They value quality and are careful shoppers, with 49% saying they are interested in functional foods like probiotics and vitamins and 72% saying they read food and beverage labels to know if the product is healthy. The majority of this generation is technologically savvy. Although some between the ages of 45 to 65 still prefer paper-based payment methods, many routinely use electronic payment options like Automated Clearing House (ACH) debits and bank online bill payment services. An estimated 43% of Boomers prefer using debit cards, while 17% have used P2P apps such as Zelle.

Boomers represent 67% of smartphone ownership and embrace the convenience of online shopping, with 53% saying they prefer shopping online over brick-and-mortar stores. An article on the Visa website states that in 2019, 40% of card-not-present Visa transactions were made by customers aged 60 to 69. The convenience of online shopping appeals to 27% of Boomers who have ordered groceries for home delivery, and for those who still prefer going to the supermarket, 41% use digital coupons while they’re grocery shopping in stores. Regardless of the shopping channel, Boomers value retailers who sell high-quality products and provide excellent customer service and attention.

Key Takeaways:

- Boomers are expected to spend 3.4% percent more on health-related purchases than their parents did.

- 59% of this age group say they are willing to pay extra for socially compliant, sustainable products.

- This demographic responds more positively to marketing messages that appeal to altruistic values rather than materialistic, “me-centered” marketing campaigns.

- They often ignore time-urgency strategies in marketing (they know there will always be another sale).

- 46% of Boomers say they rely on Cyber Monday for their holiday shopping.

- Boomers tend to gravitate toward “companies with a conscience,” and are more interested in knowing that a company honors its warranties than younger consumers.

Generation X

Generation X members were born between 1965 to 1980. Because their generation is sandwiched between the two largest demographic groups—Baby Boomers and Millennials—they tend to be overlooked by retailers, and there is less market data relating to their buying habits. But even though they represent only about 25% of the population, Gen X consumers are known to be the biggest spenders across all demographics. They make more online purchases than any other generation and 20% more than Millennials.

Generation X spends the most annually on their homes among any generation (almost $23,000), but that amounts to only 33% of total annual spending. With an average age of 43—which is 16 years older than the average Millennial—more than three in five Gen X adults own their homes rather than rent. Not only do they spend a large amount on housing, this demographic likes to eat out—a lot. In a 2017 survey by the Charles Schwab company, 66% said they regularly spend money on eating at the “hottest restaurant” in their towns. Data compiled by Marketingcharts.com from 2018 shows that this group spends about $4,229 annually on food outside the home.

When they’re not spending money on restaurant meals, this group shops more conservatively than most other generations. They tend to be risk-averse and cautious, spending a lot of time conducting research, reading online product reviews, and reviewing social media posts before deciding whether to make a purchase. They appreciate straightforward product and pricing information and when they find something they like, they are the most brand-loyal customers of all generations.

The majority of Gen X adults are married with an average of 2.5 children, and many live in a multi-generational household. Many of the older members of this generation have not only assumed the role of primary caregiver for one or more of their Boomer parents, but 52% of them also support their adult Millennial children, which may explain why they are so price-conscious.

The majority of Gen X consumers own smartphones and nearly half use mobile payment apps to make purchases. This group uses credit cards more than any other generation, but only 42% pay off their credit card balances in full each month so they are more likely to have credit card debt than other generations. Up to 49% prefer using debit cards, but since they are comfortable with technology they’re willing to replace their physical wallets with digital versions. As much as 25% of this demographic is already using P2P options.

Key Takeaways:

- This group makes more online purchases than any other generation.

- Gen X consumers find advertising to be nothing more than a way to get them to buy something, so retailers must be able to show that they understand how their products can meet their needs.

- This demographic is fond of do-it-yourself projects, and research shows that nearly 73% percent regularly watch YouTube videos on home repair and improvement, cooking, technology use and repair, arts and crafts, and beauty/personal care. Small businesses can take advantage of this trend by effectively positioning products and services in these categories to Gen X consumers.

- Facebook is this generation’s favorite social media platform, so retailers should make sure to include a link to a Facebook page on their websites.

- Gen X consumers tend to be more brand loyal than other generations, so retailers should reinforce that loyalty with free offers, bonus programs, and coupons.

- Like Boomers, Gen X shoppers put a high value on customer service and quality products and services.

- Email marketing is the preferred channel by about 80% of this demographic. They are busy with careers and families and won’t spend time reading long messages, so short, fact-based content with a clear call to action work best.

Generation Y (Millennials)

This group of people born between 1981 and 1997 has replaced Baby Boomers as the largest age demographic in the U.S. Commonly known as Millennials, they currently number over 83 million and their buying power is enormous, spending about $600 billion in the U.S. each year. According to Ad Age magazine, this generation is predicted to spend $10 trillion over their lifetime. Social and environmental responsibility is important to Millennials and they expect the companies they buy from to also reflect those values in their business practices.

Millennials grew up with technology and they’re the group leading the digital wallet revolution. They are also the group most likely to use cryptocurrencies like Bitcoin. They make heavy use of their mobile devices and are avid online shoppers— 54% of all their purchases are made online, and 63% of Millennials make purchases with their smartphones—with only 11% saying they prefer to shop in a physical store. Over half of Millennials say they use credit or debit cards when making purchases of less than $5 (debit cards in particular), and up to 23% percent use contactless payment methods at least once a week.

Although this demographic has tremendous buying power because of its sheer numbers, Millennials are hampered by debt and tight cash flow: as much as 52% carryover credit card balances month to month, 66% have one or more long-term debts, and 48% report they live paycheck to paycheck. On top of that, Millennials as a whole owe more than $1 trillion in student loan debt. This may explain why Millennials tend to focus on price, coupons, and discounts when shopping and are not particularly brand loyal: 66% say they would switch brands if offered a 30% discount.

However, they are quite willing to spend money on comfort and convenience. According to a 2019 Forbes article, Millennials spend more per year on gas, groceries, dining out at restaurants, hobbies, electronics, and clothing than other demographic groups; but they spend less on things such as television/cable services, travel, pharmacy items, and furniture than older generations. They are also more likely to use subscription services to replace regular shopping trips to grocery stores and other physical retail outlets. According to a Reuters article, 88% of Millennials say they would consider buying online and picking up in-store to save $10 on a $50 item. Rewards programs such as free shipping are also big with Millennials. In data released by Bond Brand Loyalty, 68% of 20- to 34-year-olds said they would change where they shopped if it meant getting more rewards. And one third reported buying something they didn’t necessarily want, just to earn rewards.

Key Takeaways:

- 75% are willing to pay more for great customer experiences compared to only 69% of Gen Z shoppers.

- Social and environmental responsibility influence their purchasing decisions.

- One in five Millennials surveyed relies exclusively on smartphones and tablets for online access, which means that having a mobile-optimized website is essential for a business.

- Millennial shoppers expect to find the same products (including any discounts) whether online or in the store, so retailers should make sure the shopping experience across all consumer touchpoints is consistent.

- 74% of Millennials would switch to a different retailer or brand if they had a negative customer service experience.

- Millennials are receptive to online advertising that is restrained, targeted and relevant, but only 6% think online advertising is credible.

- Social media is how most Millennials find and discover new products, so it’s important for retailers to make social media a part of their marketing strategy.

Generation Z

This demographic, sometimes referred to as Centennials, represents people born from the late 1998 to around 2010. A 2019 McKinsey & Company report notes that nine out of ten Gen Z consumers believe companies they buy from should be ethical and transparent in all aspects of their business, and have a responsibility to address environmental and social issues. As of this year, Gen Z will be the largest consumer group in the world and it’s predicted to account for 40% of global consumers. Despite their young age, Generation Z holds $44 billion in buying power, with 75% spending more than half their monthly income.

This generation never knew what the world was like before digital devices and high-speed Internet. Although 74% of Gen Z members spend most of their free time online, they are reluctant to give up personal information online because they have grown up in the era of high-profile data breaches. Less than a third is comfortable sharing personal details other than contact information and purchase history, and only 18% are willing to share payment information, even on the websites of their favorite brands. 43% of Gen Z shoppers prefer brands that provide clear terms and conditions in how they will use their information. A full 75% of this generation use mobile devices and smartphones with 25% spending more than five hours per day on their phones.

When making purchases, 14% of Gen Z shoppers prefer to pay with a credit card, 58% prefer using a debit card, and almost none use cash. For digital natives like this generation, one might assume they would prefer making online purchases, but fully 65% to 75% of Gen Z shoppers prefer in-store purchases. When they do shop online, 33% expect to be able to pick up their items at a physical store and 48% expect to be able to exchange or return online purchases at the store. Regardless of the type of shopping channel, Gen Z values product availability, quality products, and efficient service over flash and hype. They want real value for their money and expect to receive discounts and loyalty rewards programs.

Key Takeaways:

- Social media channels are extremely important to this age group and they routinely consult their community and gather opinions before buying. In addition, 41% say they have been influenced by Facebook ads.

- Product value is much more important to Gen Z than brand loyalty. When it comes to brand preferences, 45% of Gen Z consumers choose brands that are eco-friendly and socially responsible.

- Gen Z is very price conscious and focuses on the overall value when making buying decisions.

- Customer experience is everything to this generation. They are “eye-level” shoppers who put a high value on the ability to touch, feel, and interact with products, so signage and merchandise display need to catch their attention.

- Gen Z consumers want a seamless shopping experience with the ability to go from viewing a product online to going to the store to make a purchase, so retailers should ensure that their websites are SEO optimized to enable searches conducted on multiple devices.

- This generation is proud of what they purchase and likes to share pictures and comments on social media about the things they buy. Merchants should encourage them to share their positive experiences by offering a reward (“Tweet about your experience in our store today and receive a 10% discount on your next purchase!”).