The Traditional Merchant Onboarding Process vs. the PayFac Model

To fully understand the benefits of the payment facilitator model, it’s important to first take a look at what goes into creating a standard payment processing agreement. In a traditional onboarding process with an Independent Sales Organization (ISO), the merchant must first sign a direct agreement with a processing bank. The merchant interacts directly with the ISO and follows their set processes to register and become approved to accept payments. This enrollment and onboarding process often entails a great deal of paperwork and can take days or even weeks to complete. During this time, the merchant is thoroughly vetted through a Know Your Customer (KYC) program that verifies identity, ensures compliance with legal requirements, and assesses risk. In the meantime, the ISV or VAR is hoping that the merchant has a positive experience and does not experience any frustrations that could impact the relationship.

The PayFac Advantage

By contrast, the payment facilitator model eliminates the need for merchants to interface with the processor. Instead, merchants are onboarded and registered by the PayFac—bringing ISVs, SaaS businesses, and developers more control over their merchant’s onboarding and processing experience. To become a PayFac, the ISV or VAR signs a direct agreement with a processing bank (e.g., Elavon or Fiserv) to process payments on behalf of their merchant clients. Merchants can then tap into the payment facilitator’s existing relationships with acquiring banks and the PayFac’s processing technology to get up and running fast.

|

|

|

|---|---|

|

Traditional |

In a traditional model, merchant clients follow the ISO’s onboarding processes in order to register to accept payments. |

|

PayFac |

By interacting directly with their clients, PayFacs enjoy more control of their customers’ onboarding and processing experience. |

|

|

|

|---|---|

|

Traditional |

Since the ISO underwrites merchants, they bear the burden of risk when it comes to fraud, chargebacks, and PCI compliance. |

|

PayFac |

Because the acquiring bank underwrites the payment facilitator instead of the merchant, the PayFac assumes liability for all financial risk on behalf of its merchants. |

|

|

|

|---|---|

|

Traditional |

Merchants undergo a detailed analysis to verify the business’s identity, evaluate potential risk, and ensure the business maintains the necessary compliance requirements. This process can take days or weeks to complete. |

|

PayFac |

The payment facilitator undergoes the lengthy onboarding process—not the merchant. To become approved, the merchant provides a few key data points to the payment facilitator. The information is then evaluated by an underwriting tool, and the application is either approved or declined in real time. The whole process can be completed in minutes. |

|

|

|

|---|---|

|

Traditional |

Traditional payment processing fees are generally charged using the interchange plus model. With this system, rates are variable since every processed transaction qualifies for a specific rate category. Rates change based on the type of business the merchant conducts, schedules and rules provided by the card brands, as well as a number of other factors. But even though rates do change, there is rate optimization technology that can work on the merchant’s behalf to reduce their costs. |

|

PayFac |

PayFac models have a simple and transparent flat-rate fee structure, without the variability of traditional payment models. Merchants benefit from predictable costs and easy budgeting. |

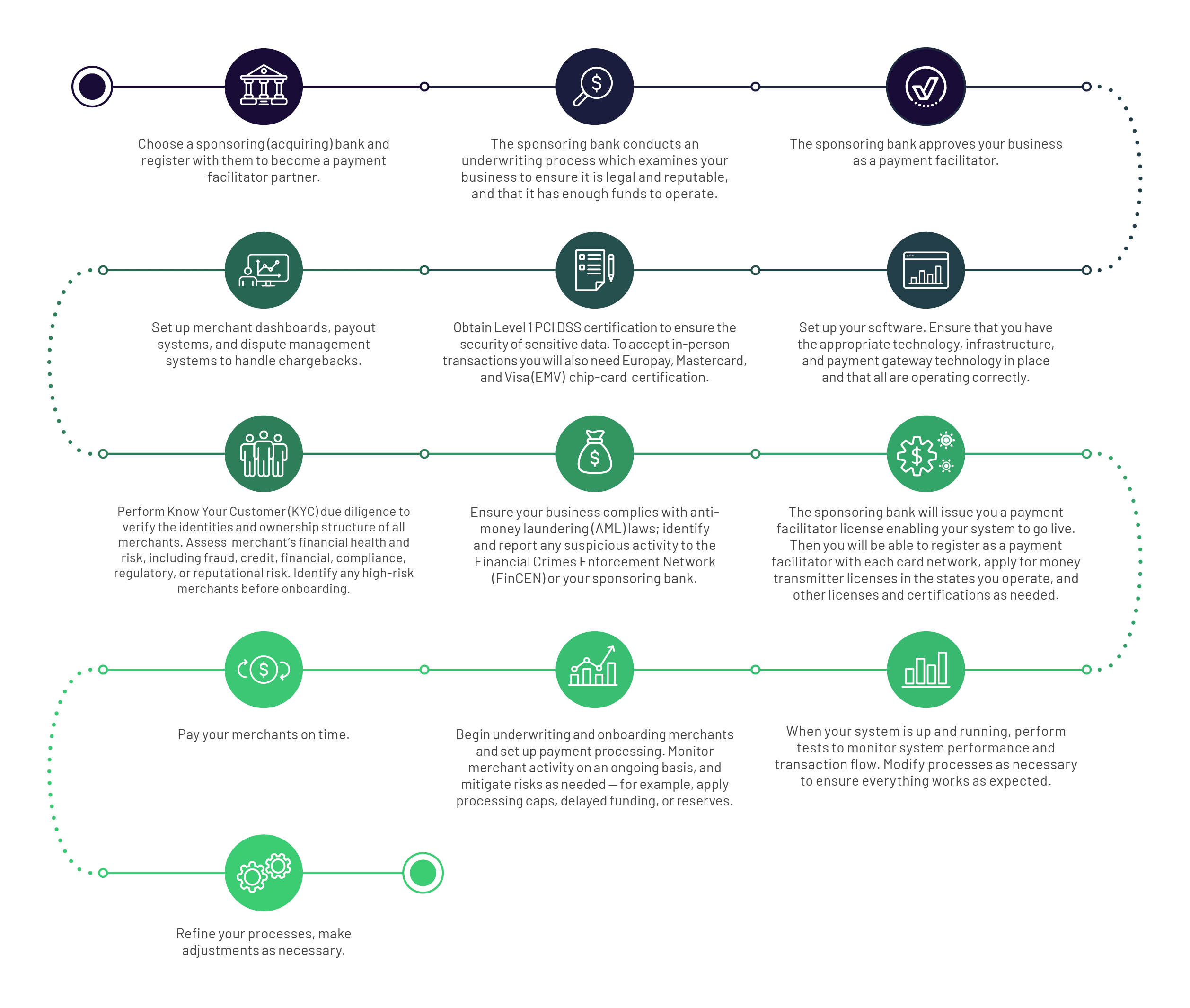

You’ve researched your industry verticals, analyzed costs and profit potential, and now understand the financial risks and responsibilities you will be taking on. If you decide that becoming a payment facilitator is right for your business, here’s an overview of how the traditional process works and what you should be prepared to do.