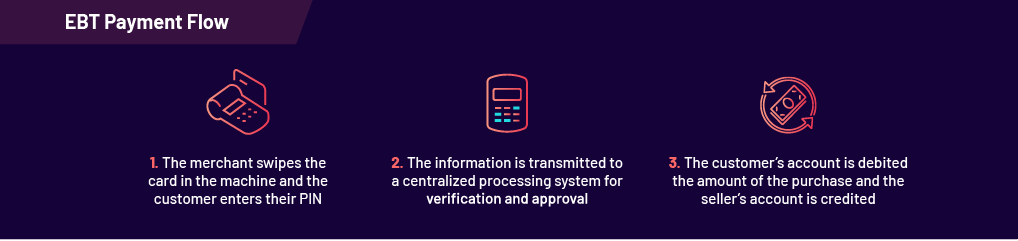

EBT payments are relatively simple since they function on the same principles as debit card payment systems. First, the merchant swipes the card in the machine and the customer enters their PIN. The information is transmitted to a centralized processing system that verifies the PIN and the amount in the user’s account, and then sends back an approval. Once the account verification and approval is completed, the customer’s account is debited the amount of the purchase and the seller’s account is credited. At the end of the day, statements are “settled,” in which funds move out of the buyer’s account and into escrow. Merchants usually get access to these funds within two business days.

EBT payments aren’t one single, monolithic payment system. There are several different government-funded programs that link to EBT cards. The two largest programs are:

1. WIC

According to the official U.S. Government Benefits Program, WIC (Women, Infants, and Children) is dedicated to providing financial support for women and children who may be at nutritional risk. In 2010, the Healthy, Hunger-Free Kids Act mandated that all WIC State Agencies adopt an electronic benefit transfer (EBT) system. State deadlines have rolled out in stages over the past 10 years, and all states are expected to have implemented EBT processing by the end of 2020.

2. SNAP

The Supplemental Nutrition Assistance Program (SNAP), as the Center on Budget and Policy Priorities (CBPP) informs us, is also known as the Food Stamp system, and has been instrumental in providing funds to ensure that over 40 million low-income American families can have food on the table.

Besides for SNAP and WIC, there is also the TANF program, or Temporary Assistance for Needy Families. This program provides financial assistance to low-income families with children.

In response to the widespread impact of the global COVID-19 pandemic, SNAP and WIC have become even more critical to the country’s well-being. Merchants who form the backbone of the economy need to address the increased number of buyers possibly invested in using the EBT system. In this paper, we’ll explore the implementation of an EBT system, and why it’s such a significant concern for merchants. Before we delve into that, however, we’ll look at each of these benefit programs in detail to get a feel for the clients who may use them.

As technology has advanced, many low-income families have turned to online shopping. To cope with this trend, the FNS has introduced a pilot program for online purchases of SNAP goods using EBT. At the time of this writing, 44 states have joined the SNAP Online Purchasing Pilot and only a handful of large retailers are supported. However, with the pilot program’s establishment, the FNS has also opened the door to other SNAP-certified businesses to register as online retailers.

Once clients start using their EBT cards to pay for goods, the process is similar to accepting a debit or credit card for payment. However, things are very different online. Whereas users can enter their PIN on a keypad in-store, they do not have this option online. As such, merchants who want to implement this service need an online PIN entry system that is secure yet easy to execute on the business’s existing e-commerce platform. Luckily, Sola has developed a dedicated online PIN entry system that integrates seamlessly with leading e-commerce platforms. Users can safely enter their EBT PIN at checkout, and the merchant’s business will receive payments similar to if someone were to make a credit or debit card purchase online.

SNAP and WIC payments moving online have created a need for digital processing services to handle these cards. Some merchants who have been using the standalone eWIC terminals have expressed their dissatisfaction with the service. Additionally, merchants who want to start accepting SNAP EBT online have been searching for a simple solution to integrate into their e-commerce platforms. Sola answered this call by creating a single software development kit (SDK) that developers can rely on to help build solutions to these problems.

In-Store SNAP Processing

To leverage your in-store terminal to process EBT payments, Sola has provided an SDK that integrates with a wide range of grocery POS systems. Customers using EBT cards for SNAP purchases can swipe their cards in the same terminal that is used for debit and credit card processing.

Sola’s API provides gateway emulators and simple code to ensure that processing happens in the blink of an eye. With a little smart programming, a standard POS terminal can process EBT payments like any other type of card.

SNAP Online EBT Processing

As SNAP retailers start moving their businesses online, they need a reliable method of accepting EBT payments with PIN entry. Naturally, most e-commerce systems don’t come with built-in functionality for online PIN entry. Sola provides an API that integrates seamlessly with many grocery e-commerce systems to enable online PIN entry— among other benefits like robust security, competitive rates, and much more.

Sola’s tools don’t limit payments to EBT cards only; they cover a wide range of alternative payment options for clients. Online grocery retailers can also depend upon advanced security features like tokenization and fraud prevention tools. Sola’s solutions minimize merchants’ processing costs while ensuring that customer payment data remains secure throughout the entire process.

In-Store eWIC Processing

Sola is an eWIC certified payment solution that merchants can rely on. The gateway we offer to clients demonstrates full integration with existing POS systems with a minimum of fuss. Once Sola’s processing is refitted onto a POS terminal, it can start accepting eWIC cards just like other credit or debit cards.

All of this can be done from a single terminal, reducing the amount of hardware that the merchant needs to have present. The transactions that a merchant completes through their POS terminal with eWIC cards are registered alongside all other purchases and can be monitored in the merchant’s POS system or in the Sola Merchant Portal virtual terminal solution. This single source of payments means that all records and bookkeeping are updated without the need for manual entry of eWIC transaction data.

As a certified eWIC payment solution, Sola has a responsibility to its merchants who decide to use the service. Part of that responsibility is the dedication to keeping our firmware up to date. If changes occur within the eWIC system, we roll out updates to users as soon as possible to keep processing smooth.

We also update our support in line with eWIC’s Approved Product List (APL). This list changes over time as items are added and removed from it with each legislation cycle. Our dedication to updating the list ensures that your transactions always use the most current APL version, without any effort on your part.