3DS technology was first developed in 1999 by Arcot Systems (now CA Technologies, a Broadcom Company) as a way to prevent unauthorized credit card transactions made online. 3D stands for “three domains.” The first domain is the card issuer, the second is the retailer receiving the payment, and the third is the 3DS infrastructure platform that acts as a secure go-between for the consumer and the retailer.

Visa was the first of the card brands to deploy 3DS technology, with the introduction of Verified by Visa in 2001. The other card brands followed suit, rolling out their own branded solutions like Mastercard SecureCode and American Express SafeKey. All of these solutions have improved e-commerce security by requiring more than just a credit card number, CVV, and address to make an online purchase. During the checkout process, the cardholder is redirected to the issuing bank’s website where they are asked to provide proof of identity by entering a unique password, an SMS code, or a temporary PIN. If the authentication process is successful, then the buyer is redirected back to the merchant’s site for payment confirmation.

With 3DS2, authentication takes place behind the scenes — usually without the customer’s involvement. The payment gateway passes along customer- and transaction-specific data points to the cardholder’s issuing bank. If the bank successfully verifies the customer’s identity and decides that the transaction poses a low fraud risk, then they authorize the transaction. In the unlikely event that the bank is unable to authenticate the cardholder’s identity with the provided data points, the cardholder may be prompted to enter their preset password for verification purposes.

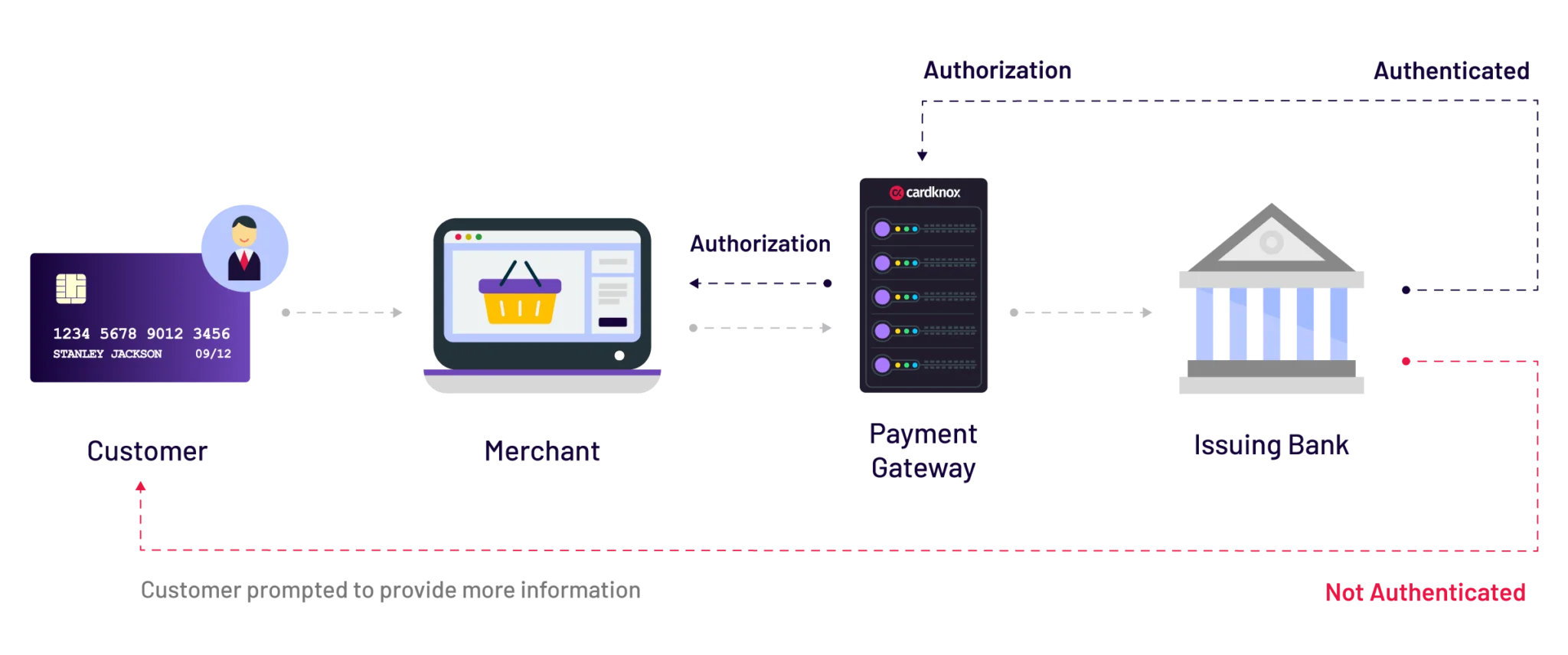

The 3-D Secure 2.0 Authentication Process

- The customer initiates a transaction online

- The payment gateway passes key data points along to the cardholder’s issuing bank so that they can evaluate risk.

- If the issuing bank successfully authenticates the customer’s identity and decides that the transaction poses a low fraud risk, then the transaction is authorized. This is the case with the majority of 3-D Secure transactions. Note: when this occurs, the merchant is not held liable if the transaction turns out to be fraudulent; the issuer would be liable instead.

- If the issuing bank was unable to authenticate the cardholder’s identity per the above steps, the cardholder will be prompted to provide more information. The issuing bank will then choose whether or not to authenticate the transaction.

The benefits of 3DS2 are clear for merchants and consumers alike, and the adoption of 3DS2 is picking up steam in the payment and retail spaces. Now’s the time to start supporting this advanced technology!

If you’re a merchant or developer who’s looking to get started with 3DS2 technology, know that Sola offers the easiest and most cutting-edge path. Choose from our payment gateway integrations for e-commerce sites, or use the PaymentSITE hosted checkout form for a sleek checkout flow that requires zero development work.

The Role of Sola in 3DS2 Authentication

As a payment gateway, Sola supports the technical infrastructure and the relationships required for the secure processing of payment data. The gateway operates as a facilitator between the cardholder’s bank and the merchant’s issuing bank. This central role allows Sola to gather and pass along key data points to the card brand for authentication.

Sola E-Commerce Integrations

Sola is a leader in developer-friendly payment gateway integrations for accepting payments online, in-store, and through mobile devices. Our support for 3DS2 allows you to streamline e-commerce and mobile payment flows to ensure customer satisfaction while safeguarding cardholder data.

The Sola payment gateway was created by developers for developers. Many Sola integrations can be completed with just a few lines of code. To ensure that integration is hassle-free, our white-glove integrations support team is available to assist.

Choose between a full integration of our payment gateway for your website using our powerful API, plugins for popular shopping carts, or a quick migration from an existing solution using our gateway emulators:

Custom Integrations: Our comprehensive SDK provides the tools you need to integrate faster, including a full-stack API that enables deep integration and a custom payment flow.

Plugins for Popular Shopping Carts: Sola provides easy-to-use plugins for WooCommerce Magento, and other leading online shopping carts. Using our proprietary iFields solution, sensitive card data completely bypasses the host server, significantly reducing your PCI scope and liability.

Gateway Emulators: Our gateway emulators will translate your existing gateway’s API into Sola API so that transactions can be routed through your gateway to Sola — without the need for a full integration. Simply change the gateway URL to the Sola endpoint and get up and running fast.

PaymentSITE Hosted Payment Form

Start accepting secure payments online without writing a line of code or dealing with security and hosting challenges. Sola’s hosted payment form tool, PaymentSITE, makes it easy to build customizable forms for accepting payments. PaymentSITE streamlines payment requests for donations, deposits, and invoices by giving you the capability to email your payment form, share it using a unique URL, or embed it into your webpage. Features of PaymentSITE include the ability to:

- Customize required fields for billing, shipping, and transaction info

- Support mobile wallets for one-click mobile commerce

- Curb fraud and simplify PCI compliance using robust data tokenization

- Prompt consumers to opt-in to recurring payments

- Create consistent branding with a logo upload tool

Even More Benefits of Sola E-Commerce Solutions

In addition to industry-leading 3DS2 security, you’ll enjoy access to many added features and benefits to help you streamline invoicing, improve customer satisfaction, and lower costs.

- Gain Greater Control and Efficiency with Split Capture: Rather than having to capture the total authorization amount when shipping out orders, merchants who use Split Capture are able to capture multiple portions of a prior authorization.

- Make Payments Predictable with Recurring Payments: Set up automatic payments with the ability to customize amounts and frequencies.

- Support a Wide Range of Payment Methods: Sola supports credit and debit cards (EMV, contactless, magstripe), mobile wallets, ACH, EBT, and more.

- Provide a Frictionless Checkout with Digital Wallets: It’s easy to make websites mobile-friendly with Sola’s support for digital wallets like Apple Pay and Google Pay.

- Reduce Costs with Interchange Qualification Monitoring (IQM): Sola performs over a dozen checks and routes transactions to minimize fees for merchants.

- Safeguard Your Business with Advanced Security: 3DS2 is just one of Sola’s many security features. We also offer true tokenization that assigns a unique ID for each transaction, as well as fraud filtering that stops fraud in its tracks.

- Simplify PCI Compliance: With Sola, your system never touches actual credit card data, making PCI compliance that much easier.