B2B payments are accounts payable and accounts receivable transactions between businesses. Unlike business-to-consumer (B2C) payments that are paid at the point of sale, B2B payments are typically made after the goods or services are delivered. The usual process is as follows: the customer places an order, the provider fulfills the order and sends an invoice to the purchaser, the purchaser checks the invoice against the terms of the purchase order and pays the balance, and the provider receives the payment and updates their records. Some of these steps are done manually, and the entire process usually involves several teams of employees. In sizable companies with active accounts payable and receivable — especially those that rely on physical invoices and checks — this can be time-consuming, costly, and prone to error and fraud.

Businesses make and receive payments using a wide range of payment methods, and each has its own costs, advantages, and risk profiles. Here we will briefly review their pros and cons.

Checks

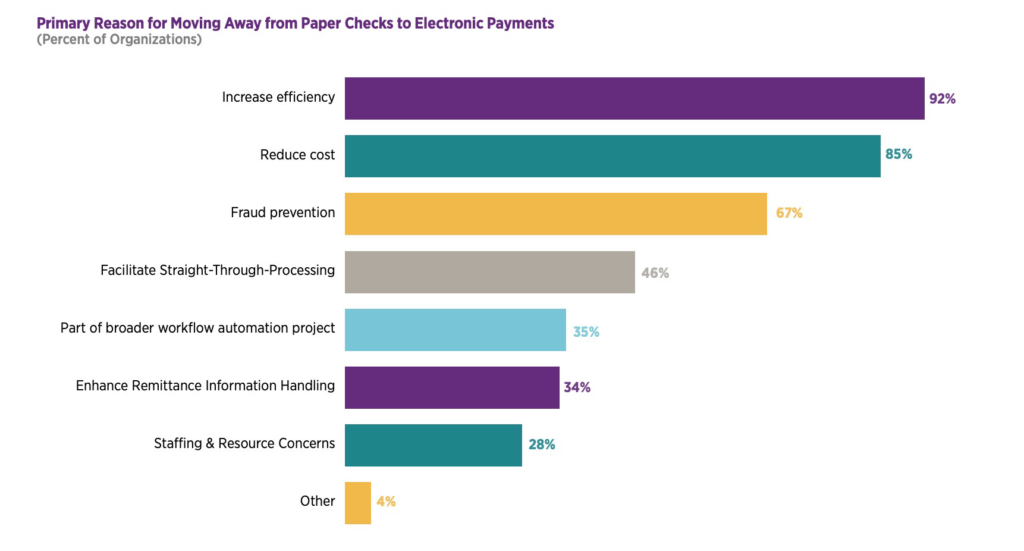

The use of checks for B2B payments remains widespread, despite their drawbacks. In 2018, checks accounted for 32.4% and 34.4% of receivables and payables transactions, respectively. However, check use is declining for a variety of reasons (see graph on page 5). The Association for Finance Professional (AFP)’s 2019 survey showed that 42% of U.S. B2B payments were made by check, down sharply from the 81% reported in 2004.

Graph 1: Primary Reason for Moving Away from Paper Checks to Electronic Payments

Automated Clearing House (ACH)

ACH payments are among the most commonly used by B2B organizations. The AFP found that 87% of its 2022 survey respondents accept ACH credit transactions and 73% accept ACH debit transactions for incoming payments, while 78% use one or the other to make outgoing payments.

The introduction of real-time payment technology is driving the growth of ACH. In 2017, The Clearing House launched RTP (Real-Time Payments) so that consumers and businesses could conveniently send ACH payments directly from their accounts at federally insured depository institutions 24/7, and receive and access funds sent to them over the RTP network immediately. In 2023, the Fed plans to launch another real-time payments system called FedNow.

Wire Transfers

Wire transfers are also electronic fund transfers from one bank account to another, but, unlike ACH transfers, a wire system such as Fedwire or The Clearing House Interbank Payments System (CHIPS) provides immediate and final settlement. This payment method is popular in the capital markets, real estate, and financial services sectors due to its high level of security.

Credit Cards

While in the past credit cards were used primarily for B2C payments, in recent years they have grown in popularity in the B2B space. In 2021, two-thirds of the companies surveyed by the AFP used credit cards for accounts receivables.

Credit cards are often used for smaller transactions, in part because of the fees they impose. The median average incoming credit card transaction from the AFP’s 2022 Payments Cost Benchmarking survey ranged between $300 and $499. Only 9% of the companies surveyed said that the average size of their credit card transactions exceeded $15,000. The median size has increased since 2015, when it ranged between $200 and $299. That could be due to companies’ desire to minimize manual transactions during the COVID-19 pandemic, along with improvements in card transaction integration with ERP, accounting, and other back-office systems.

B2B is on track to experience a technological revolution that will solve the problems listed above, among many others. In fact, a recent survey revealed that 86% of executives consider it at least moderately important to improve their current digital payment capabilities. This process has by and large already occurred for B2C payments, with 82% of Americans having reported using some form of digital payment in 2021.

While progress is lagging in the B2B industry, it is indeed occurring. Here’s a look at some of the latest trends and innovations for B2B payments:

The Shift Toward Electronic Payments

Nearly three-quarters of those surveyed in AFP’s 2022 Payments Cost Benchmarking Survey reported that they are moving from checks to electronic payments “to increase efficiency, save money, and reduce costs.” The number of firms that need to make this transition remains high, however — according to the AFP’s survey, companies made 42% of their payments by check in 2021, and 92% accepted checks for incoming transactions. Other drivers of the transition toward electronic payments include:

Real-Time Payments

According to Mastercard’s The B2B Payments Tipping Point survey from 2018, RTP has several important advantages, including:

Mastercard’s survey found that real-time payment adoption is driven mainly by the need to improve the efficiency of payment systems (83%), respond to technological innovation (69%), and reduce systemic risks (63%).

E-Commerce

Investing in e-commerce capabilities is key to staying competitive. American Express’s B2B Payment Trends To Watch In 2021 survey found that 42% of small – and medium-sized B2B businesses experienced an increase in online transactions in Q2 and Q3 of 2020, and businesses implementing e-commerce expect to see five times faster revenue growth. Forrester forecasts that B2B e-commerce in the U.S. will reach $1.8 trillion and account for 17% of all B2B sales by 2023.

Virtual Card Spending

Virtual cards are essentially one-time-use credit card numbers that link to an existing credit card. According to American Express’s B2B Payment Trends to Watch in 2021 report, virtual card spend is forecasted to grow from $213.8 billion in 2021 to $414.2 billion in 2024. This is likely due to the robust security that virtual cards provide, especially at a time when credit card fraud is on the rise — between 2019 and 2020, reports of credit card fraud for new accounts increased by an astounding 48%.