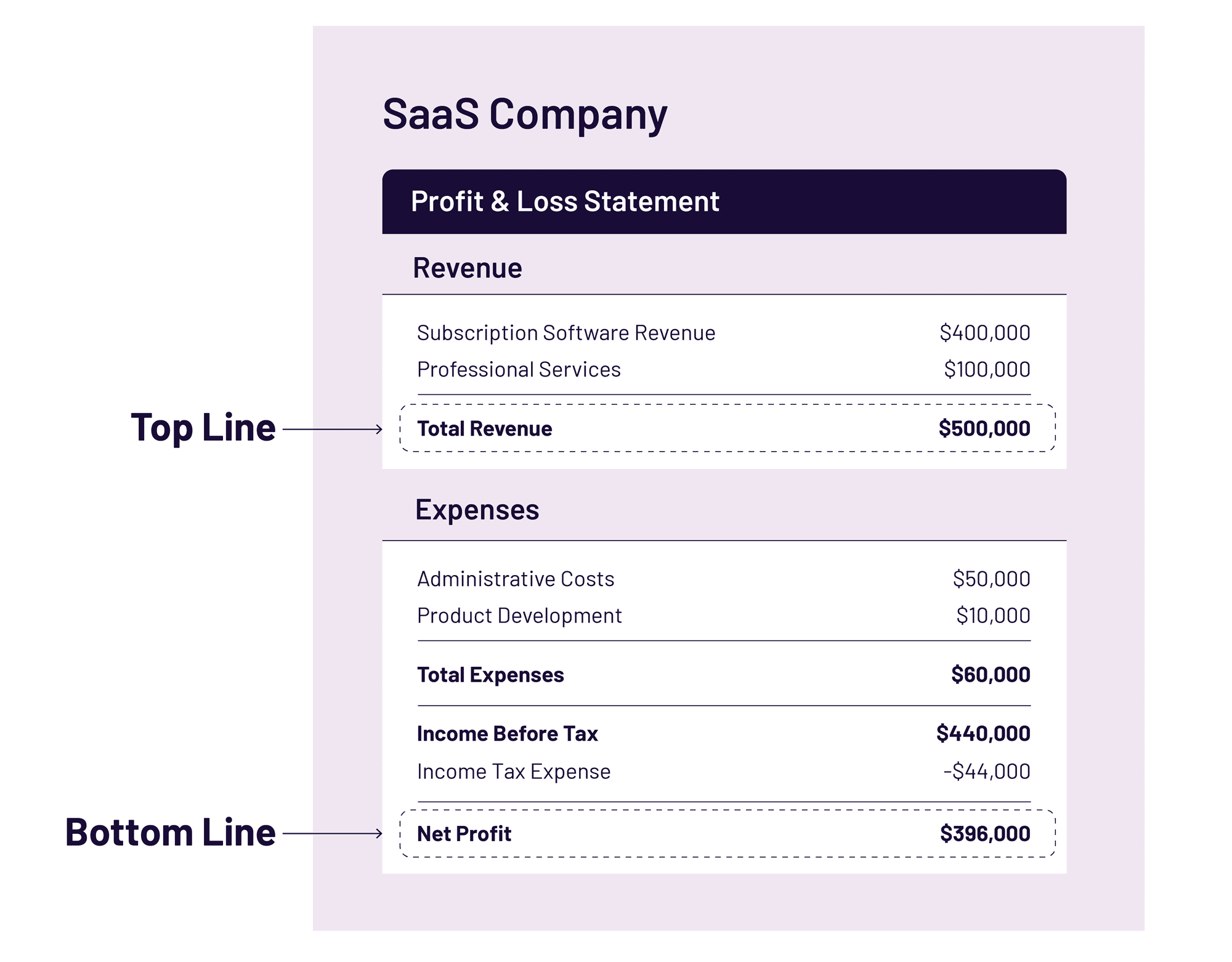

In the dynamic world of business, one term reigns supreme—the elusive “bottom line.” Shorthand for a company’s net income, the bottom line gets its name from its placement on a financial statement, which is (you guessed it!) at the bottom.

We talk less about the top line, which references the gross figures reported by a company—aka, revenue. A company that increases its revenue is said to be generating top-line growth, and that growth is a key indicator of the company’s future outlook in the marketplace.

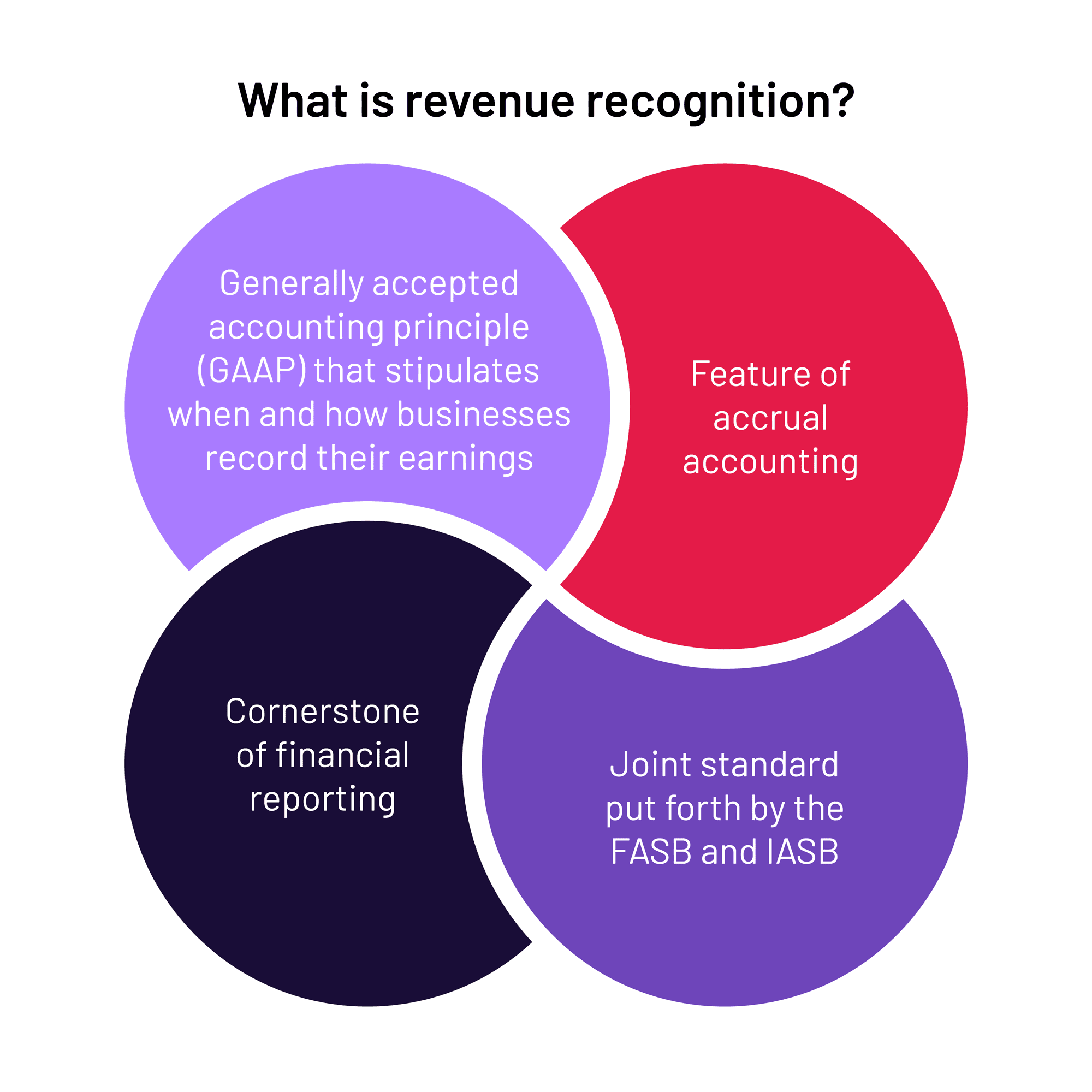

For businesses looking to fundraise, get a loan, or increase their valuation, it’s essential that they recognize and record their revenue according to best accounting practices. Although accounting may not be the most glamorous aspect of the business world, possessing a fundamental grasp of cash versus accrual is undeniably essential. This knowledge forms the bedrock for leveraging the revenue recognition principle, ultimately propelling your top line to new heights.

But what is revenue recognition, anyway? Read on to learn more about the fundamental workings of this system, how it’s regulated under U.S. guidelines, and how you can harness its power to hit performance targets and attract investors.

In the past, because global accounting policies were industry-specific, standards on when and how to recognize revenue were difficult to implement. For investors, this made it challenging to compare the performance of companies across verticals.

That’s why two regulatory boards, the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB), created a new, shared framework for revenue recognition across business models. Internationally, this framework is known as the IFRS 15. In the US, we refer to it as the ASC 606.

The FASB is responsible for maintaining Generally Accepted Accounting Principles (U.S. GAAP). Similarly, the IASB is responsible for maintaining International Financial Reporting Standards (IFRS).

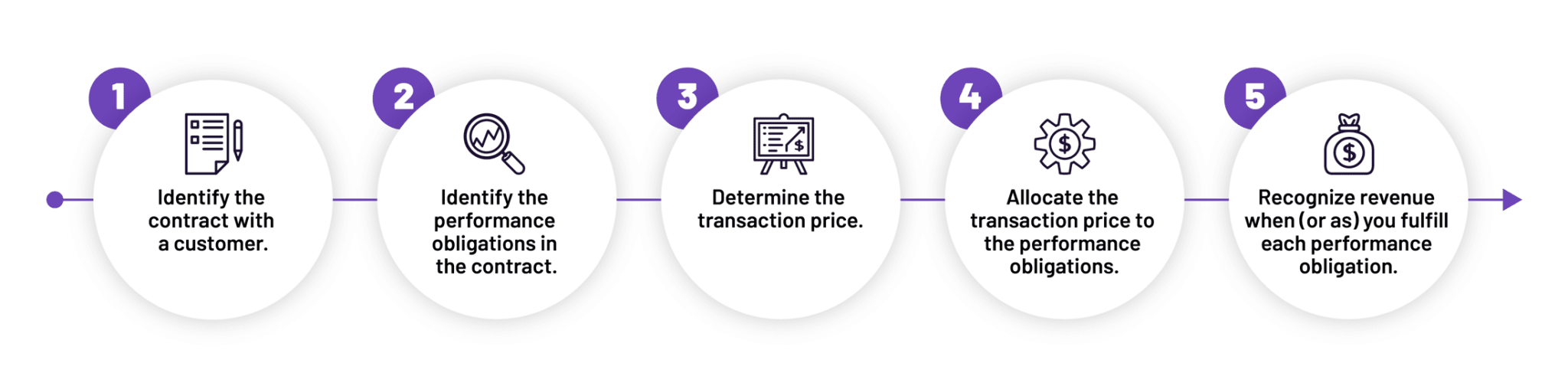

The ASC 606 standard requires businesses to adhere to a five-step revenue recognition model.

Step 1: Identify the contract with a customer.

To recognize revenue, a business must begin by identifying the contract with a customer. ASC 606 guidance defines this contract as an agreement between two or more parties. This agreement must create enforceable rights and obligations.

Step 2: Identify the performance obligations in the contract.

Next, the business must identify the performance obligation(s)—aka, the promise of the transfer of goods or services to a customer—in the contract. These performance obligations can be individual or combined, and the distinction will help determine whether the business, in accounting terms, is an agent or principal.

Step 3: Determine the transaction price.

In addition to the money exchanged with a customer, there are also variable considerations included in the transaction price, such as potential discounts or the right to return.

Step 4: Allocate the transaction price to the performance obligations.

Each performance obligation needs a specific selling price. For variable considerations, businesses are responsible for estimating the price based on expected value.

Step 5: Recognize revenue when (or as) you fulfill each performance obligation.

No revenue should be recognized until the performance obligation is complete. However, for subscription businesses, revenue can be recognized evenly throughout the service period.